When I joined my first startup in January 2008, we had two lead gen channels that actually worked: events and outbound. I came in to run events, and it was, without question, our most effective pipeline source. At the time, we didn't have sophisticated martech stacks or programmatic ad campaigns. We showed up, we met people, we tracked our leads by who took our collateral (literally printed collateral packets and stuffed them into envelopes with prospect names on them) at events, and our reps worked their networks.

Fast forward nearly twenty years, and here's what the 2026 Early-Stage GTM Report is telling us: we're back. Kind of.

This is the second annual edition of Mercury Fund's benchmarking study, and is informed by data collected from 125+ early-stage B2B software GTM leaders in Q1 2026. I spent 15+ years in B2B software GTM and below are my key findings and observations.

The Inbound Playbook Is Breaking Down

The share of early-stage teams with 75%+ inbound pipeline fell from 26% to 17% year-over-year. That matters more than it might look on paper, because inbound leads generally convert at higher rates than outbound. Make sense, someone interested in your solution who’s demonstrating interest is likely to move down funnel faster than a cold lead who doesn’t know who you are. A shrinking inbound share puts real pressure on mid-funnel performance, and you can see that in the data: Lead:MQL dropped from 41% to 32% this year.

To make up for declining inbound volume, we’re seeing pipeline coming from what I’d consider more traditional GTM levers. Events more than doubled as a primary lead source year-over-year. Outbound jumped from one of the lowest-ranked channels in 2025 to the second highest in 2026. We do see more teams leveraging AI for outbound sales and marketing campaigns: 58% in 2025 jumped to 84% this year (+25pts).

Email and paid search both declined as lead sources. The data doesn't tell us why, but my hypothesis is that buyers are getting harder to reach through digital channels. There's more noise, more AI-generated outreach, and more content competing for attention, and it's getting harder to cut through it all. Whatever the cause, early-stage teams are responding by investing in channels that require a human on the other end. Which, if you were doing GTM work in the early to mid-2000s, feels pretty familiar, except this time, with more technology to support outbounding efforts.

Teams aren’t just investing in the top performing channels, they’re hiring around them: event marketing and AEs are the most in-demand GTM hires this year.

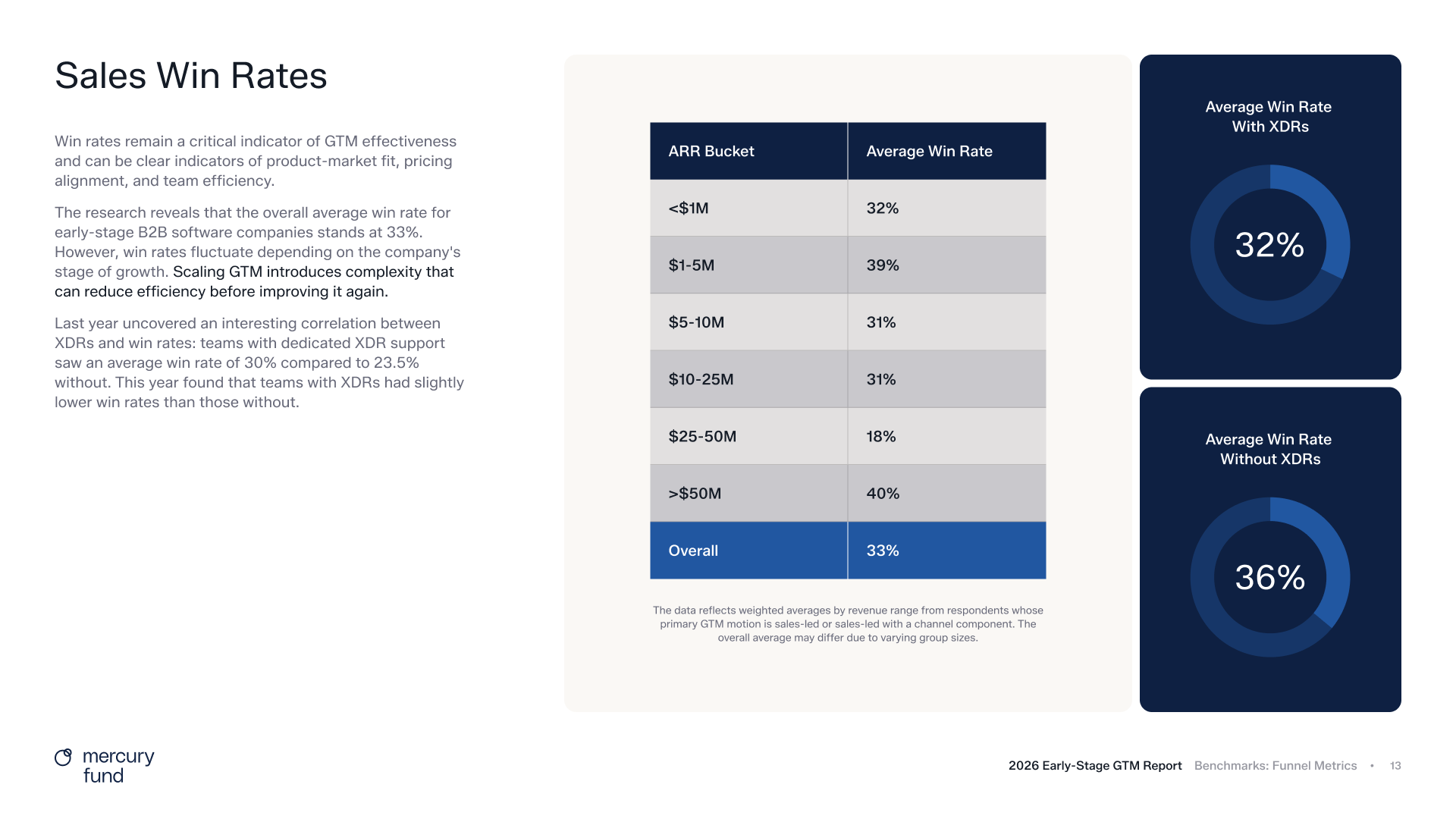

Win Rates Are Up, But the XDR Story Flipped

Overall win rates improved from 29% in 2025 to 33% in 2026, and that tracks with other signals in the data (more on that below).

But the finding that genuinely surprised me was what happened with XDRs.

Last year, we found that teams with dedicated XDR support had a meaningfully higher win rate (30.4%) than those without (23.5%). This year, the data inverted: teams without XDRs are now winning at 36%, compared to 32% for teams that have them.

I don't want to draw a firm conclusion from one year of data. My hypothesis is that this could be related to how aggressively teams are automating the SDR/BDR function with AI, which the report findings directly support: the share of companies substituting AI for SDR/BDR headcount nearly tripled, from 6.8% in 2025 to 28.8% in 2026.

If AI is handling more of what XDRs traditionally did, teams that invested heavily in that headcount may be navigating a transition of reallocating headcount to closing functions, customer-facing roles, or exiting XDRs entirely. We'll be watching this one closely to see what the data reveals next year.

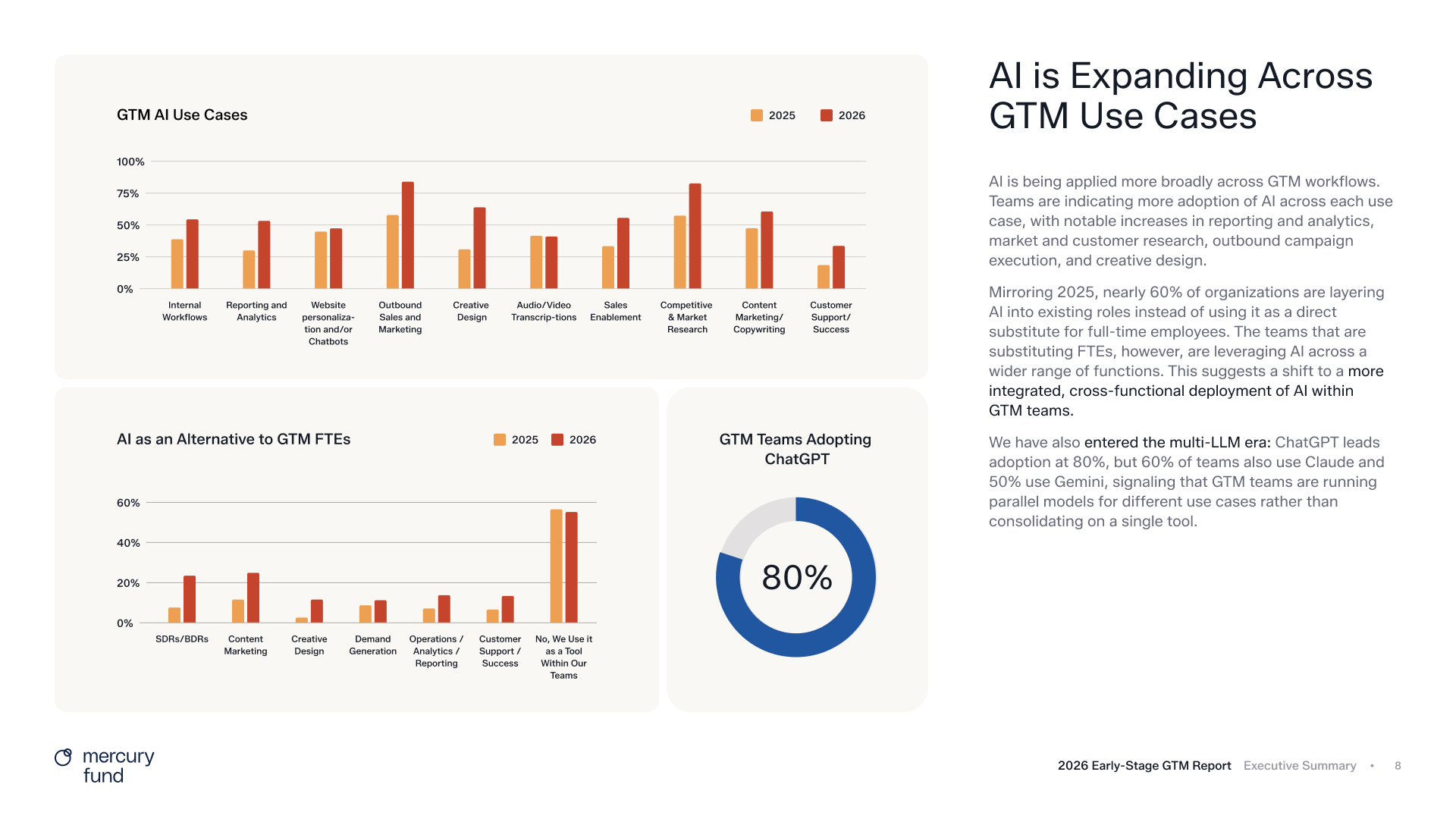

Unsurprisingly, AI Use Cases are Expanding

96% of GTM leaders now rank AI as a top or critical priority, compared to less than 60% in 2025 who called it "a top priority but not the most important”. What's striking isn't just the adoption, it's that AI use cases expanded across every single GTM function YoY, with no use case declining. The biggest jumps:

- Creative Design: 30% → 60% (+29pts)

- Outbound Sales & Marketing: 58% → 84% (+25pts)

- Reporting & Analytics: 29% → 54% (+25pts)

- Competitive & Market Research: 57% → 82% (+25pts)

- Sales Enablement: 33% → 54% (+21pts)

This tells us that teams have quickly moved beyond experimentation to AI being embedded in nearly every use case and workflow. We also see evidence of this in tool adoption, where ChatGPT jumped to the #1 spot with 80% of respondents using it. Interestingly, 60% of teams also use Claude and 50% use Gemini, signaling that teams may be running parallel models for different use cases rather than consolidating on a single tool.

Hiring decisions reflect the use case patterns. For example, we see a decrease in Content Marketing roles on marketing teams today, and fewer than 10% of teams plan to hire Content Marketing in 2026. Of note, 25% of sales teams and 36% of marketing do not plan to add headcount in 2026.

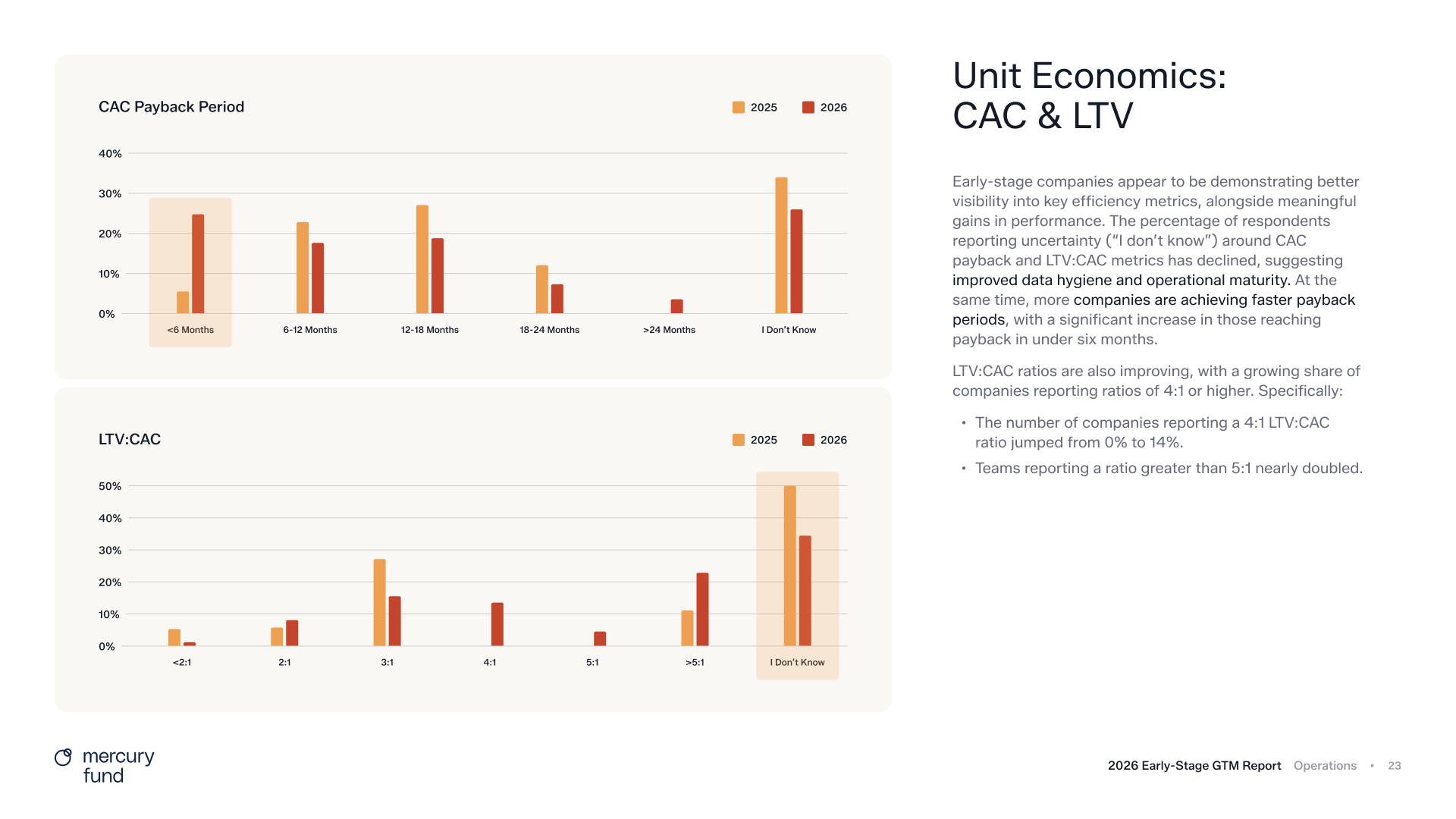

Capital Efficiency Is Improving, And Teams Are Measuring It

Last year, we advocated for the importance of consistently measuring and tracking unit economic metrics like CAC payback periods, LTV:CAC and other key funnel metrics like deal cycle velocity. I was happy to see fewer respondents said they "don't know" their CAC payback or LTV:CAC, which tells me operational and data maturity is improving across the board.

In terms of findings:

- CAC payback under six months grew fivefold year-over-year. ← this is huge!

- Companies reporting a 4:1 LTV:CAC ratio jumped from 0% to 14%.

- ACV concentration shifted into the $30–50K range, up from $5–15K in 2025.

- Sales cycles of 160+ days have nearly disappeared.

The data is telling us that larger sized deals are moving through the funnel faster, and the time to recoup the costs to acquire a customer is shrinking. This is pretty incredible and every GTM exec’s dream scenario.

The improvement in deal velocity and contract value could suggest buyers are coming in more qualified and more decisive, which would be a downstream effect of teams getting more disciplined about ICP and outbound targeting. We love to see hyper diligence in segmentation and messaging, and for those efforts to be paying off. This is just a hypothesis, but obviously one we’re going to continue to test and track.

What We're Paying Attention to in 2027

The through-line across all of this, to me, is that the playbooks that carried B2B SaaS GTM for the last decade are being stress-tested. Inbound is softening, digital channels are noisy, AI is compressing headcount in some functions while other roles are seeing more demand, and some of the ‘traditional’ channels, like events, are back.

We'll keep surveying, keep benchmarking, and keep sharing what we find.

The report also dives into operational design, processes, and tooling. We recommend taking a look through it, and we’d love to hear your thoughts!